understanding investing

and how to ride out bad markets

“a fool and his money are lucky enough to get together in the first place, sport.”

-gordon gekko

“if lessons in finance were cheap, more people would understand finance”

-el gato malo

the world is a funny place. there are many fields in which one may possess talent or expertise and such attainments or endowments inevitably confer advantage in the pursuit of whatever the goals of that field happen to be.

what’s interesting is the way that “the amateurs” view “the pros” in any given area of endeavor. at the one margin, few want to kibitz or try their own hand at brain surgery or semiconductor design or playing the oboe or flying a jet fighter. people have no idea how to even start thinking about those things and as such (wisely) avoid doing them.

on the other end of the spectrum, you have ideas like “investing” where john q public and jane m basic have been led to think “i know stuff! i’m good at this!” but mostly, they aren’t.

sorry, but this is true and most of the ‘great democratization of investing and trading” is one long series of “cheese in mousetraps” to lure the unsuspecting onto “free trading” platforms that feed your net wealth into the scalping machines of citadel, jump, and XTX. “hey, maybe you’ll be really good at blackjack!” the pitboss leers. “the rules are simple, here’s a card to tell you when to hit and some free chips to get you started.” a year later you’re degen yoloing ZDE options on companies whose name you just learned for the first time this morning.

it’s a nasty trap because the other side of this issue is that in the easy money era of “money printer go brrrrrrr” bubble concatenation (which began and has been accelerating since 2000) if you are not in “assets” best of luck keeping your wealth up with the joneses. more or less, you have to play. and as the great kenny said:

“if you’re gonna play the game boy, you gotta learn to play it right.”

so, in the vein of such ideas, let’s talk about how people do it wrong.

first, debt. honestly, i cannot improve upon this speech from kevin spacey as frank underwood in “house of cards.”

this should be shown to every high school kid in america once a week.

this is 101 stuff that i would wager that 70% of people get wrong and around which vast cargo cults have been erected to convince people that “expensive college is an investment.”

for some, it might be. you spend money, you get a degree that provides valuable skills that you can put to work for good pay, and the cash on cash return is excellent. but that’s really only for a certain sort of person and there is always a price beyond which it stops making sense. “$200k in education” might pay off for the top decile. for the middle percentile? you probably wanted a different product and if you’re going to run that up pursuing an independent major in the intersectional grievances of marginalized gender theory in precolumbian peruvian pottery, brace for a life of the very debt slavery oppression you have been taught to so abhor. it’s like watching someone focus so hard on worrying about a pothole that they drive right into it. small wonder they wind up so angry…

bottom line is that debt is obligation and you need to pay it. it’s also leverage and leverage can kill, especially when looking at equities and real estate. i watched one of the richest familes i knew, people who owned an actual castle that they had had taken apart in europe and flown to the US and reassembled go BK in 2008 because they were massively leveraged in commercial real estate.

i’ve seen i have no idea how many investors and traders get carried out on high gearing bets.

if you are not a professional, don’t use margin. even the pros die that way. if you buy an equity or an asset, it has value and if it drops in price, no one will come and take it from you. but if you lever up, they will. margin calls come at the worst possible times. they make you sell when you should be buying or holding because you doubled down so a 30-50% loss gets you liquidated in totality.

this matters in volatile markets and in bad bears.

the quick buck is tempting, but you generally want to leave that one alone.

but here’s the biggest mindset issue that get around:

let me explain the difference between a professional investor and “retail.”

a stock is a claim on the assets and cash flows of a company. if you realize that, then (assuming those things remain sound) when the price of the stock declines, it becomes more attractive for you to buy. that is the professional/serious view of investing. when it goes “on sale” you see it as more attractive to purchase. (note that we’re talking about “investing” here, not trading)

most “retail” investors claim to know this, but don’t. their mindset is mostly self-deception.

here’s why:

they are not actually buying a claim on a company, they are buying a stock price.

it’s really that simple and everything else emerges from that.

stock go up? yay! i’m brilliant and my thesis is correct. i’ll run around finding confirming data and believing everything good i see about the company and ignore that bad.

if people tell me i’m wrong, i’ll smirk and reply “stock price, bro!”

but “stock go down”? now the thing you bought is broken. it was supposed to go up, but instead you lost money. this gets you emotional and it inverts the process of confirmation bias from the one you had when you were winning. you now seek out every bad piece of data about a company and believe it. you ignore the good.

“stock price bro!” gets yelled at you from friends and validated in red ink. there must be something wrong. obviously all the bad things are right.

at this point, you’re cooked. your process is fundamentally broken.

you are not a pingpong player, you’re a pingpong ball.

in the end, win or lose, you are not trying to price a company, you are playing “pin the confirmation bias on the stock price.”

you bought a price and if it performs well, you make up a happy story and if it trades badly, you make up a story of failure (or, my personal favorite, “market manipulation” or those notorious rascals the “naked shorts.”)

one needs to learn to separate a couple of concepts. in the long run, fundamentals drive stock prices, but at any given moment in time, the stock price is not “the fundamentals” it’s “a story about the fundamentals,” and stories and reality can diverge markedly.

this is why markets move the way they do in surges and dogpiles. the price does not reflect the fundamentals, through an emotive cycle of confirmation bias, the price determines the story about the fundamentals and causes feedback loops.

stock go up, story good, so stock go up, so story good.

stock go down, story bad, so stock go down, so story bad.

but you can only run a positive feedback loop so far (often much further than people suspect) before it pops.

one of the ways to time the inflection on this is to look for story/performance divergence. when a stock announces good news and trades badly, you’re in trouble. the story has gotten too good for reality. when a stock reports bad news and trades well, you’ve likely priced in more bad story than fits reality.

most people will spend their lives buying tops and selling bottoms. everyone knows to “buy low, sell high” and “when everyone else is a seller be the buyer” but almost no one can actually do this. it’s emotionally harrowing. when everything you buy loses money, the buy button starts to feel like touching a hot stove. when everything you sell keeps going up, the FOMO gets too intense to resist.

then it peaks, rolls over, and now “you’ll sell when it goes back to the highs” and it drops more and now you’re “just waiting for the bear raid to end” or “the relief rally” but when it comes now you think you’re going back to the highs etc. late stage addict behavior is obsession over technical analysis and backfit and trying to map elliot waves onto things and using post facto validation to pretend that every “reverse duck and feathers” pattern on the chart would always validate on the far right hand side. (it never does, it’s modern day haruspicy.)

so you get dragged down in choppy moves until the price has dropped so much that you tell yourself the “bad story” about how “something must be wrong” because “the stock is down.”

maybe it is. maybe it isn’t. that’s the thing to figure out. if you want to be a trader, then you need to trade like one and get out fast when you’re wrong about price. but if you want to be an investor, you have to start from fundamentals and then develop an opinion about what something is worth and what you’d pay for it. opinions span years, not days

there are other ways to make money, good ways. trading, arbitrage, etc. but if you’re going to go play there, realize you’re trying to compete with brain surgeons on brain surgery and that they have a huge embedded advantage from technology, size, training, and links to markets and credit with which you cannot compete and win.

investing is the best plan for most people and the core axiom is simple:

if you let price decide your view of the fundamentals, you’re going to be a part of the whipsaw.

you need to let the fundamentals decide what constitutes an attractive price to own an asset, know what you own and why you own it, and revise your price targets based on fundamentals, not price action.

at the margin, if you do not like an investment more when the price drops, you’re not an investor.

similarly, if a stock extends past what you think is fair value, your thesis is now “greater fool” and that’s a thesis you can play (as stocks often overshoot), but you better know you’re playing it.

where the really nasty trouble starts is when pricing becomes opaque and manipulated. this is actually very difficult in public markets (at least for long) and history is littered with the exploded remains of people who tried to corner some commodity market, but in assets for which there is no market price, things are very different.

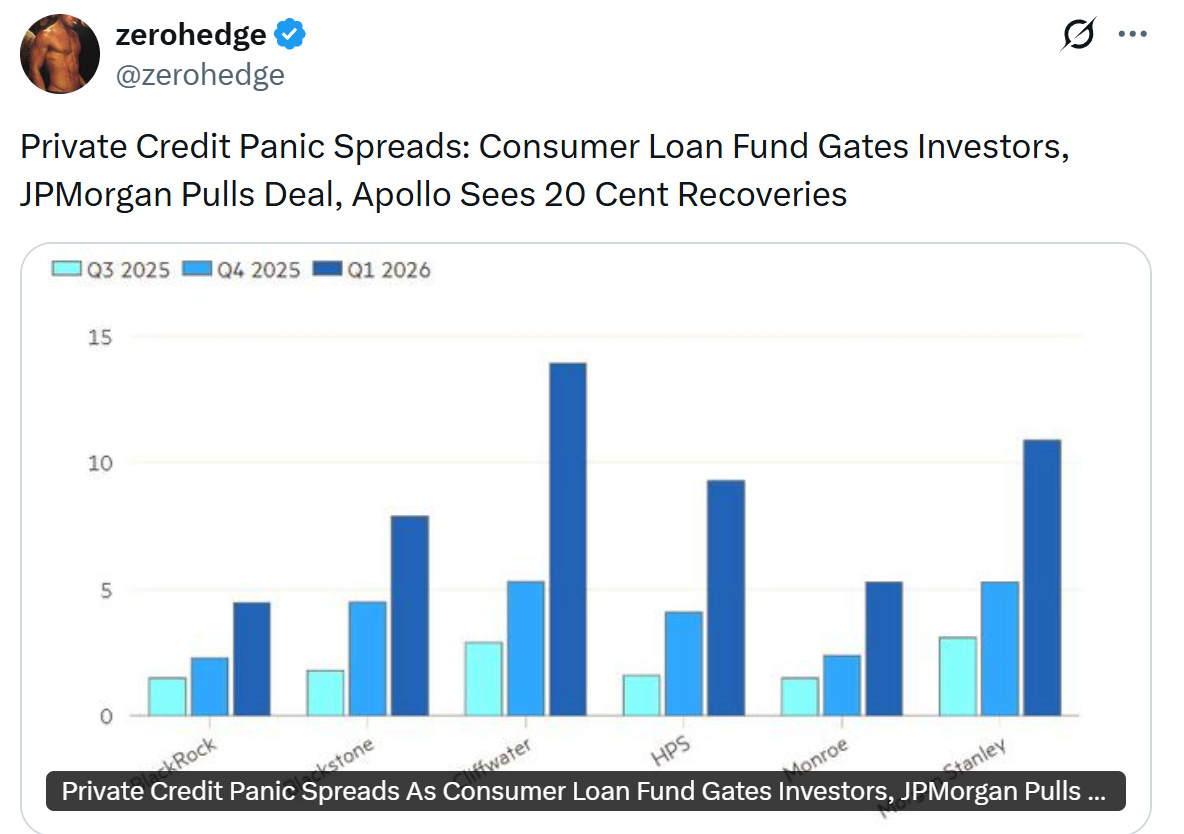

the current bugbear is “private credit.”

most are not familiar with this market. it’s basically credit funds, pools of assets that lend to (often early stage) companies that lack the credit histories and cash flow to get bank loans. it’s higher risk, higher rate money that also gets called “venture lending” and like most interesting ideas in finance, it was started by some clever boots folks who saw an inefficiency and said “these guys will borrow at 15% and give us an upside warrant kicker and we can drive 20% IRR’s in this space and the equity funder is sequoia and they will not let it go bust. they’ll pay us back before they let us grab the asset in a default.

it was a great play, lots of folks made lots of money, and then the trade got crowded as more and more entrants piled in, AUM in the space exploded to what is likely $1-1.2tn in the US, some estimate $1.6tn for 2025, but it’s a surprisingly difficult asset class to size. everyone is in from the banks to blackstone to apollo to fido the wonder dog.

investors loved the returns to these funds. high rates, low volatility, great stuff. made the portfolio look tickety boo. they got packed into endowments and retirement funds.

the problem is the “price” of the loans is made up. it’s a “mark” in a space infamous for “extend and pretend” and for the crackhead accommodations of “we’re going to PIK” (payment in kind) where the debt is no longer being paid but rather expanded. you have $100 million in debt. your rate is 14%. even an interest-only payment would be $3.5 million/quarter. but you don’t pay it. instead you just add it to the bill. now you are $103.5 million in debt. next quarter the PIK is $3.62mm and on and on. this is what frank underwood warned you about. compound interst is working against you.

i suspect a lot of these funds are in trouble, especially the ones that loaned piles of money to SaaS companies that looked like the blue chip safe space bet and are now in the AI gunsights. (and yes, that’s very real)

alone, this would likely not be enough to pose large scale systemic risk. blackstone goes $400 million into their own pocket to pay redemptions and blue owl gets kicked in the junk, so what?

the answer lies on the other end of the funding spigot: the $3-5tn US VC and PE space and the companies therein who have been the borrowers on these loans. what happens when there is no more credit to be had? ties go out and naked swimmers get revealed.

this newfound nudity is unlikely to be pretty because the health of that space is far from robust and it has become another massively overcrowded trade relying upon reporting high returns and low volatility in a space for which there is no “market price.”

and they have been playing silly buggers with that.

and eventually the buggers bugger back.

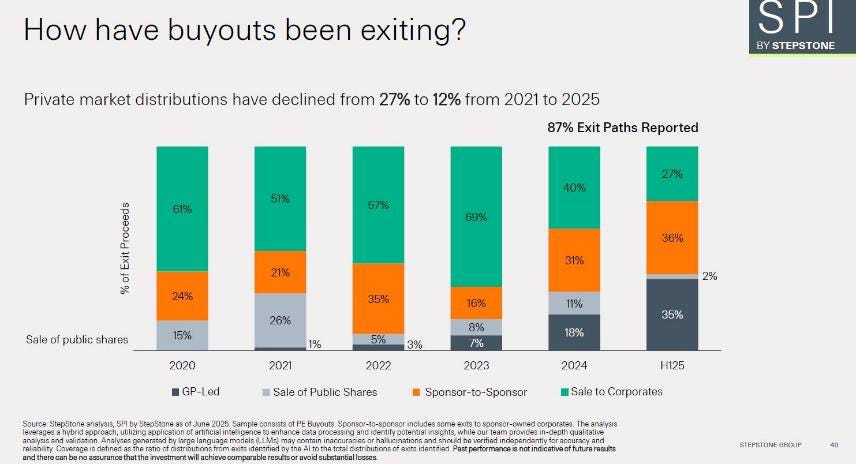

if this chart does not scare you, i fear you’re not reading it correctly yet.

private equity and VC have gone, if not full ponzi, something close enough to leave a similarly sized smoking crater.

70%+ of "exits" are just rolling the asset into a new vintage of the VC’s fund or selling it to another fund (often in exchange for buying some of their junk at similarly overblown pricing)

the venture ponziists are playing extend and pretend pass the parcel with their massive “lack of exits” portfolios.

private company values have exceeded pubcos.

why not? you can make them up. it just take one small round of cash in. no one else gets to hit that bid.

this is not price discovery, it's price manipulation.

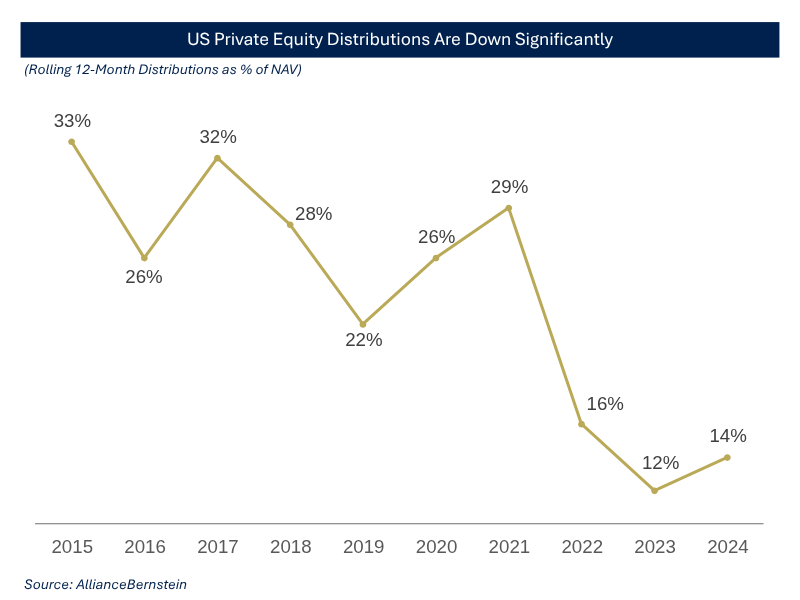

and you can see the problem in the cash flows.

distributions used to be around 1/3. now they are barely in double digits.

2025 looks to be about 13% again (but this is not out yet)

they have been painting over rust for years. and there is no out.

this whole asset class is egregiously mispriced and someone is going to get left holding the bag on a bunch of "down 70-90%" vintages.

that will be systemically important and it seems like a “when?” not an “if?”

and that will create a market that gets “sporty.”

and that is when:

you do not want to be in debt for things that cost you money

you do not want to own equities on margin

and you want to have a fundamental sense of why you own what you own and what it’s worth

then, you can shop the sales instead of being forced to be the seller and can mostly ignore the chaotic outcomes and pick and choose your places and positions.

the game of wealth creation is all about not being forced into choices but rather preserving the ability to make them and the sense to make them well.

bear markets and market calamities are inevitable.

letting them harm you in the long run is optional.

stuff will get cheap, too cheap. it’s scary and painful. but if you separate the fundamentals from the price and the story about the fundamentals, it’s where fortunes are made.

Excellent article.

Ah...retail...er...dead money. ..where money goes to die.

The stock doesn't know you own it. So you should be able to explain why you own it in less than 2 minutes. . But you can only do that if you've done your homework...as you say, gato.

Some folks will pinch pennies at the grocery store but won’t think twice about dropping $20,000 on a stock tip from a guy on the bus.

I always write down the reason I bought it, how i arrived there, and what are my selling conditions. Its been helpful squashing any "emotional attachment" I may have developed for a stock i was initially excited about.

I'm just a Carpenter. People pay me to do stuff that they cannot. I have 40 years of experience doing my job. Yes, I've seen people go bankrupt in construction, but generally because they grow too big, too fast, usually using inherited money. I may not be smart enough to invest my money, but I'm smart enough to know that. 😉 Ai will not be taking my job, and I have skills that will be valuable if "it" hits the fan.